State Sen. José Menendez and State Rep. Eddie Lucio III have introduced good companion bills (SB 2407 / HB 2507) that would implement protections for Texans against short-term health insurance policies, commonly known as “skinny plans.” These plans often do not cover basic health care needs, which can expose Texans to substantial medical debt if they get sick or injured.

Unlike comprehensive health plans, short-term plans can discriminate against people with pre-existing conditions — sometimes by denying coverage upfront.

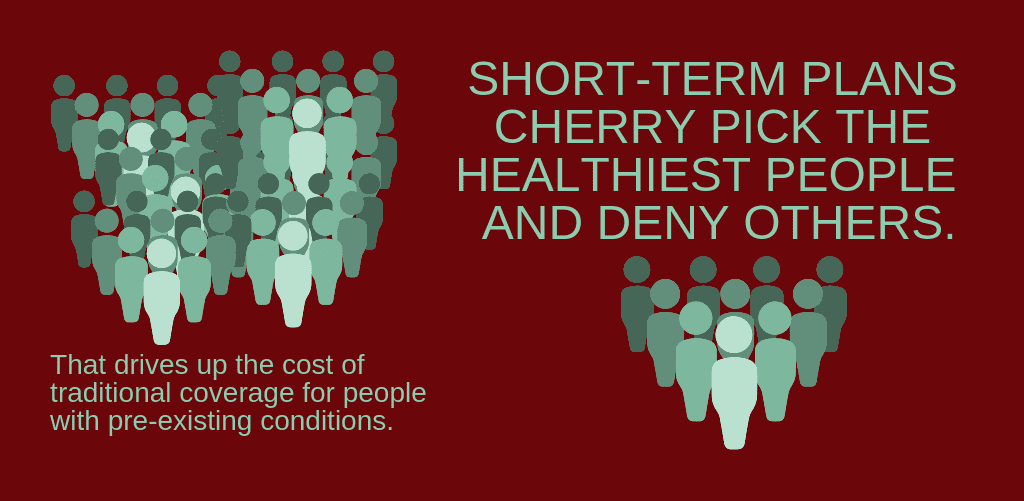

Short-term plans insurers can deny coverage to people with pre-existing conditions, and even if they sell a plan to you, they can later deny any health care they claim was related to a pre-existing condition, even if it was not diagnosed before you bought the policy. Short-term plans will cherry pick the healthiest people from the traditional insurance market and deny others, segmenting the market. Premiums for traditional health insurance that covers pre-existing conditions will rise and consumers’ options will decrease, as the pool of people who stay in the traditional market becomes more expensive on average.

Short-term health insurance plans were originally designed as a temporary measure to prevent a gap in coverage during a brief transition period: for example when a worker is changing employers, or a young adult becomes ineligible for coverage under their parents’ plan and is searching for their own insurance. Until recently, these plans could provide coverage for a maximum of three months. Unfortunately, new changes to federal regulations now allow these skinny plans to last up to one year — with the option to extend coverage for up to three years.

Fortunately, SB 2407 / HB 2507 would return the length of short-term plans to three

Under these bills, short-term plans would also have to improve disclosures, to help consumers understand the limits of what they are buying. For example, plans would have to list whether they cover essential health needs that many skinny plans often do not cover including:

• prescription drug coverage;

• mental health services;

• substance use disorder treatment;

• maternity care; hospitalization

• surgery;

• emergency health care; and

• preventive health care.

Twenty-four other states have placed limits on the sale of short-term plans to better protect consumers. Twenty of these states, including Oklahoma, South Dakota, and Indiana, allow short-term plans to fill gaps in coverage but limit the length of short-term plan contracts to less than a year. Four other states have effectively banned short-term health plans.

Many patient and consumer groups support this legislation including AARP, American Diabetes Association, American Heart Association, Leukemia & Lymphoma Society, National Multiple Sclerosis Society, and the National Alliance on Mental Illness Texas.

Short-term plans can offer real value by bridging temporary gaps in coverage, but if these plans are allowed to function as a skimpy long-term coverage option, they will only add to the problems of medical debt and uncompensated care.

The Texas Legislature should pass these bills as quickly as possible because they empower and protect consumers of health

CPPP Health & Wellness Intern Kevin P. Caudill wrote this piece.